DeFi Interest Rates Comparison: Why Fixed Rates Win for Real-Economy Borrowers

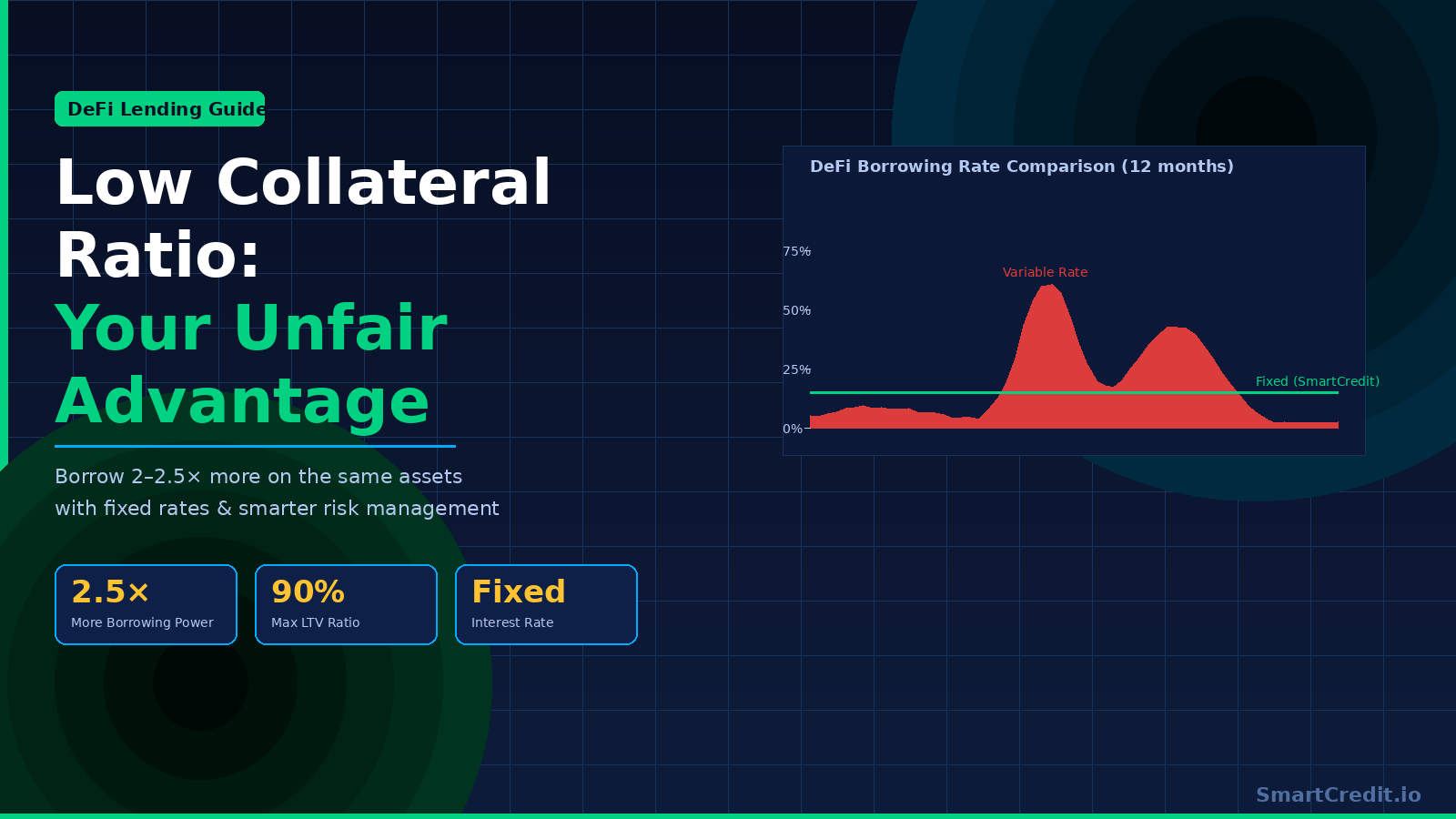

Fixed vs variable DeFi rates: SmartCredit.io offers 8-15% fixed APY (predictable) vs Aave/Compound 3-35% variable (volatile). Real data (5-year analysis): Aave USDC rates ranged 3.2% to 38.7% (1,109% volatility). SmartCredit fixed rates: 8-12% (0% volatility). Who benefits from fixed: (1) Real-economy borrowers – budgeting requires certainty, (2) Traders – leveraged positions need predictable costs, (3) Lenders – stable income planning. Who needs variable: Speculators timing short-term rate dips. March 2025 example: Variable rates spiked 12% в†’ 35% in 48 hours. Fixed users locked 10%, saved 25%. Immunebytes audited, non-custodial. Visit