Over $20 billion is currently earning yield in DeFi lending protocols worldwide вҖ” and most of it is locked into products that pay variable rates, custody your assets, or demand collateral ratios so high that your capital sits wasted. SmartCredit.io was built differently: fixed rates, non-custodial, and up to 90% LTV вҖ” with nine distinct strategies that let you earn whether youвҖҷre a holder, lender, borrower, or affiliate.

This guide breaks down every earning strategy available on SmartCredit.io, from the simplest (stake and earn) to the most powerful (leveraged staking at 2xвҖ“5x Lido APY), with real APY ranges, honest trade-offs, and exactly how to get started.

Non-custodial. No KYC. Fixed rates locked at the start. Choose your strategy below and put your crypto to work today.

Open SmartCredit.io App вҶ’

SmartCredit.io at a Glance: Why Earning Here Is Different

Before diving into the nine strategies, itвҖҷs worth understanding what makes SmartCredit.ioвҖҷs earning model structurally different from platforms like Aave, Compound, or Nexo.

Fixed rates, not variable ones. When you lend on SmartCredit.io, you agree to a fixed rate for a fixed term. You know exactly what youвҖҷll earn before you commit a single dollar. On Aave or Compound, your lending rate can drop from 8% to 1% overnight depending on pool utilisation. Our deep-dive DeFi Interest Rates Comparison covers five years of live data showing just how volatile variable rates really are.

Peer-to-peer architecture, not pool-to-pool. SmartCredit.io matches individual lenders with individual borrowers. There is no liquidity pool absorbing your funds and repricing your return. Your capital goes to a specific loan at a specific rate вҖ” and thatвҖҷs the rate you earn.

Multiple simultaneous income layers. On most platforms, you earn one thing: either interest or token rewards. On SmartCredit.io, you can stack interest income, SMARTCREDIT bonus rewards, staking yields on those rewards, and referral income вҖ” all at the same time. That stacking is what drives the headline APY numbers.

Non-custodial by design. You control your private keys. SmartCredit.io cannot access your funds. This is a structural security guarantee, not a marketing promise.

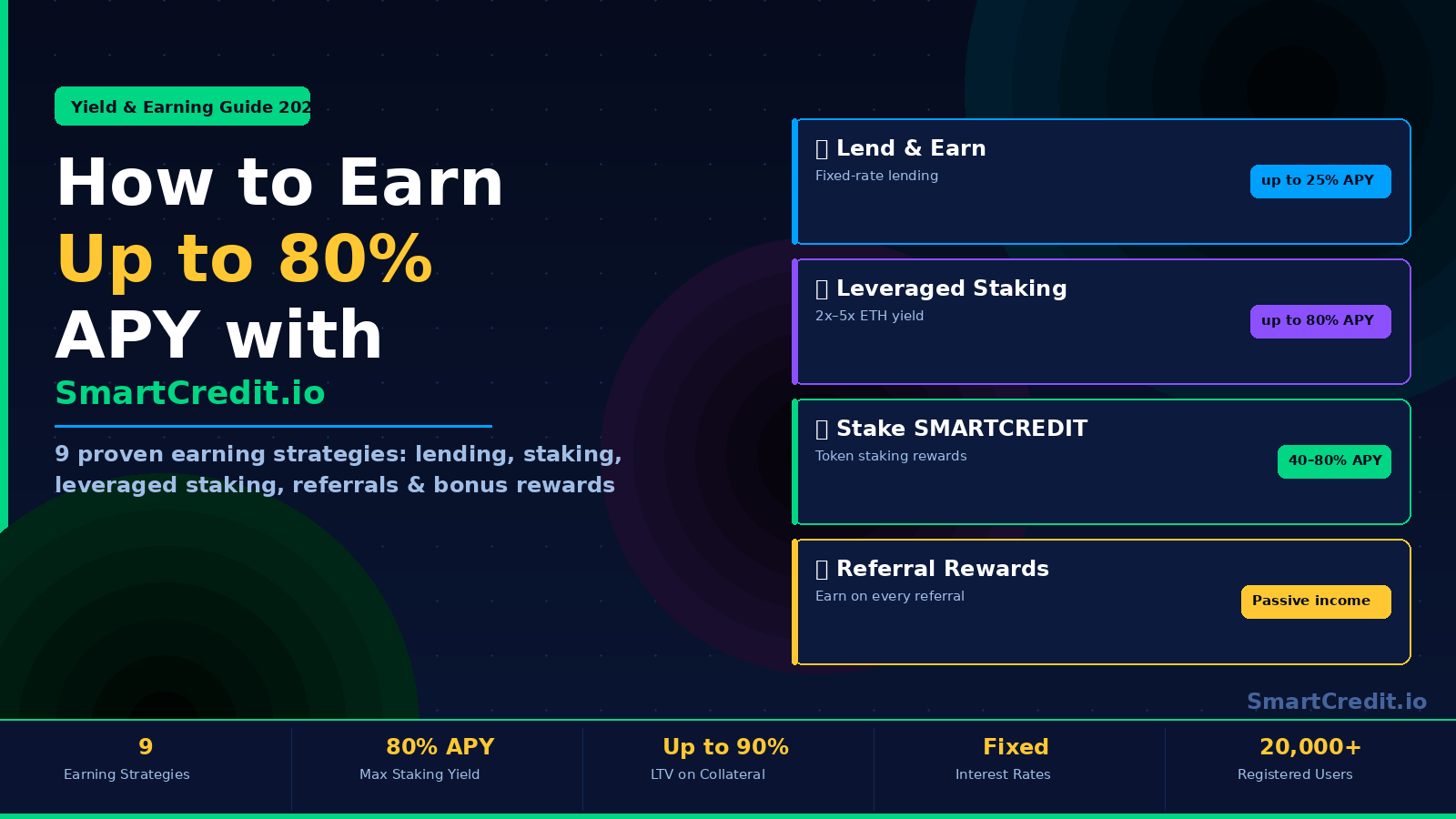

Overview: All 9 Earning Strategies at a Glance

| # | Strategy | Best For | Approx. APY | Complexity |

|---|---|---|---|---|

| 1 | Borrow вҶ’ Earn Bonus Rewards вҶ’ Stake Rewards | Active borrowers | ~15% APY (net) | вҳ…вҳ…вҳҶвҳҶвҳҶ |

| 2 | Lend вҶ’ Earn Bonus Rewards вҶ’ Stake Rewards | Passive income seekers | ~33% APY | вҳ…вҳ…вҳҶвҳҶвҳҶ |

| 3 | Borrow вҶ’ Buy SMARTCREDIT вҶ’ Stake | Higher-yield seekers | 55вҖ“60% APY | вҳ…вҳ…вҳ…вҳҶвҳҶ |

| 4 | Monetize Collateral вҶ’ Buy SMARTCREDIT вҶ’ Stake | Long-term holders | 17вҖ“21% APY | вҳ…вҳ…вҳ…вҳҶвҳҶ |

| 5 | Borrow вҶ’ Earn SMARTCREDIT Bonus Rewards | Simple borrowers | 10вҖ“20% APY (net) | вҳ…вҳҶвҳҶвҳҶвҳҶ |

| 6 | Lend вҶ’ Earn Interest + Bonus Rewards | Conservative lenders | 25вҖ“30% APY | вҳ…вҳҶвҳҶвҳҶвҳҶ |

| 7 | Stake SMARTCREDIT Tokens | Token holders | 40вҖ“80% APY | вҳ…вҳҶвҳҶвҳҶвҳҶ |

| 8 | First Loan Reward (50 SMARTCREDIT) | New borrowers | One-time bonus | вҳ…вҳҶвҳҶвҳҶвҳҶ |

| 9 | Referral Program (25 SMARTCREDIT/referral) | Community builders | Ongoing passive | вҳ…вҳҶвҳҶвҳҶвҳҶ |

APY figures assume a stable SMARTCREDIT price and are based on platform parameters at time of writing. Actual returns depend on platform volume, reward caps, and SMARTCREDIT market price. Not investment advice.

The Power Strategies (Strategies 1вҖ“4)

Strategy 1: Borrow, Earn Bonus Rewards, and Stake the Rewards (~15% Net APY)

This strategy turns borrowing itself into a net yield position вҖ” something that simply doesnвҖҷt exist on traditional DeFi platforms.

HereвҖҷs how it works step by step:

- Borrow on SmartCredit.io against your ETH, BTC, or stablecoin collateral at a fixed rate.

- Receive weekly SMARTCREDIT bonus rewards allocated every Sunday at 12:00 UTC. These rewards are claimable immediately via the вҖңMy RewardsвҖқ screen.

- Stake those weekly rewards into a SMARTCREDIT staking position to compound your returns.

- Use gas-less re-staking to reinvest staking rewards without paying Ethereum transaction fees.

- At loan maturity, repay principal and interest вҖ” and keep the net yield from rewards minus interest cost.

Net result: Approximately 15% APY after interest costs, assuming stable SMARTCREDIT price and a total platform borrowing volume below $5M. A key advantage: gas fees are only charged on your first borrowing transaction. All subsequent borrows are gas-free.

Strategy 2: Lend, Earn Bonus Rewards, and Stake the Rewards (~33% APY)

For lenders, SmartCredit.ioвҖҷs layered earning model produces returns that fixed-income DeFi products simply cannot match. This is the most popular strategy for passive income seekers.

- Lend stablecoins or ETH via SmartCredit.ioвҖҷs Fixed Income Funds (FIFs) at a fixed rate for a fixed term.

- Receive weekly SMARTCREDIT bonus rewards on top of your fixed interest income.

- Stake those bonus rewards immediately via the вҖңMy RewardsвҖқ screen.

- Use gas-less re-staking every week to compound without fees.

Net result: Approximately 33% APY combining fixed interest income and SMARTCREDIT reward staking. This is a conservative, lender-side strategy with predictable base returns вҖ” the bonus rewards simply amplify them significantly. To understand how our Fixed Income Funds work in depth, see our guide on Best Crypto Lending Platforms 2025.

Lend stablecoins or ETH at a fixed rate, collect weekly SMARTCREDIT bonus rewards, and stack both income streams simultaneously. No rate surprises. No custody risk.

Start Lending вҶ’

Strategy 3: Borrow, Buy SMARTCREDIT, Earn Rewards, and Stake (55вҖ“60% APY)

This is SmartCredit.ioвҖҷs highest-yield strategy for active participants who want to maximise exposure to the SMARTCREDIT ecosystem.

- Borrow for a longer term вҖ” ETH at approximately 2% APY or stablecoins at 6вҖ“9% APY fixed.

- Use the borrowed funds to purchase SMARTCREDIT tokens via 1inch or another DEX.

- Stake the purchased SMARTCREDIT tokens to earn 40вҖ“80% APY in staking rewards. Important: staking rewards become claimable 90 days after deposit. Withdrawing before 90 days forfeits rewards, so commit only for the full term.

- Earn weekly borrowing bonus rewards on top of the staking income вҖ” these are claimable immediately.

- Add weekly bonus rewards to your staking position via gas-less re-staking.

- At loan maturity, repay the principal and interest.

Net result: 55вҖ“60% APY assuming stable SMARTCREDIT price. The leverage here is not price leverage вҖ” it is yield leverage. You are using cheap, fixed-rate debt to access higher-yield staking returns, with the spread representing your net gain.

Key risk factor: This strategy is sensitive to SMARTCREDIT price. A significant drop in token price during the loan term would reduce or eliminate the net yield advantage. Always size this position relative to your risk tolerance.

Strategy 4: Monetize Collateral via Borrowing, Buy SMARTCREDIT, Stake (17вҖ“21% APY)

Strategy 4 is the long-term holderвҖҷs answer to idle collateral. If you already hold ETH, wBTC, or other supported assets as long-term investments, this strategy puts your collateral to work without selling a single token.

Supported collateral tokens include ETH, wETH, wBTC, USDC, USDT, DAI, LINK, UNI, MKR, and SMARTCREDIT itself, among others.

- Borrow against your existing collateral for a longer fixed term and earn bonus rewards for the borrowing.

- Use borrowed stablecoins to purchase SMARTCREDIT via 1inch.

- Stake SMARTCREDIT and earn 40вҖ“80% APY in staking rewards (rewards claimable after 90-day lock).

- Add weekly bonus rewards to your staking position via gas-less re-staking.

- Repay loan principal and interest at maturity.

Net result: 17вҖ“21% APY on your total collateral USD value. This is a conservative implementation of the Strategy 3 model вҖ” appropriate for holders who want yield without selling or significantly increasing their risk profile. Want to understand how collateral works across DeFi? Read our complete guide on Using Crypto as Collateral for Loans.

The Foundation Strategies (Strategies 5вҖ“7)

Strategy 5: Borrow and Earn SMARTCREDIT Bonus Rewards (10вҖ“20% Net APY)

The simplest borrower-side earning strategy. Borrow any supported asset on SmartCredit.io and receive weekly SMARTCREDIT bonus rewards automatically. No additional steps required.

The bonus reward APY typically ranges from 10вҖ“50% annualised depending on total platform borrowing volume. When platform borrowing is below $5M, rewards are higher. As volume grows, they dilute вҖ” a standard liquidity incentive mechanism. Net of interest costs, expect 10вҖ“20% APY on your borrowed amount returned as SMARTCREDIT tokens.

Strategy 6: Lend, Earn Interest, and Earn SMARTCREDIT Bonus Rewards (25вҖ“30% APY)

The simplest lender-side strategy. Deposit into a Fixed Income Fund and earn two income streams simultaneously: fixed lending interest and weekly SMARTCREDIT bonus rewards.

Fixed Income Funds let you define your investment rules вҖ” which maturities you want to lend into, minimum acceptable interest rates вҖ” and the platform automatically matches your capital to borrowers meeting your criteria. This results in a combined yield of 25вҖ“30% APY without any active management on your part.

For those interested in how DeFi fixed income compares to traditional bond markets, see our analysis of Crypto Fixed Income and SmartCredit.io.

Strategy 7: Stake SMARTCREDIT and Earn Staking Rewards (40вҖ“80% APY)

The purest token-holder strategy. If you already hold SMARTCREDIT tokens, staking them generates 40вҖ“80% APY in additional SMARTCREDIT rewards вҖ” entirely passive, no borrowing or lending required.

How it works: 4,327 SMARTCREDIT tokens are distributed weekly to all stakers, proportional to their staked share. The fewer total stakers in the pool, the higher each individual stakerвҖҷs share вҖ” which means early stakers benefit most. Rewards become claimable 90 days after deposit, and gas-less re-staking allows compounding without transaction fees.

Hold SMARTCREDIT tokens? Put them to work. Weekly rewards distributed to all stakers, with gas-less compounding and no active management required.

Start Staking вҶ’

Bonus Strategies (Strategies 8вҖ“9)

Strategy 8: First Loan Reward вҖ” 50 SMARTCREDIT Tokens

New to SmartCredit.io? Your first loan of more than $1,000 earns you an instant 50 SMARTCREDIT token reward, claimable immediately via the вҖңMy RewardsвҖқ screen. This is a one-time onboarding bonus available when the campaign is active вҖ” designed to give new borrowers a head start on their staking or reinvestment journey.

Strategy 9: Referral Program вҖ” 25 SMARTCREDIT Per Referral + Ongoing Fees

SmartCredit.ioвҖҷs affiliate program is one of the most generous in DeFi. When someone uses your referral link and completes their first loan of more than $1,000, you earn:

- 25 SMARTCREDIT tokens вҖ” claimable immediately via the вҖңMy RewardsвҖқ screen.

- 50% of all loan origination fees generated by that referral, forever. This creates compounding passive income from every active borrower you bring to the platform.

Affiliates can embed SmartCredit.ioвҖҷs borrowing and lending widgets directly on their websites, allowing seamless in-page conversions. Referral links work via social media, email, or any content channel.

The Bonus Strategy Nobody Talks About: Leveraged Lido Staking

Beyond the nine core strategies above, SmartCredit.io offers one of DeFiвҖҷs most innovative yield products: Fixed Rate Leveraged Lido Staking.

Instead of earning 1x the standard Lido ETH staking APY, this product lets you earn 2x, 3x, 4x, or 5x вҖ” by using stETH as collateral to borrow more ETH, re-stake it, and loop the position up to five times. The entire loop is automated. The interest rate is fixed for a 180-day term. And SmartCredit.ioвҖҷs proprietary Liquidation Probability Calculator вҖ” built on financial mathematics similar to options pricing вҖ” shows you the exact probability of liquidation before you open any position.

Even at 5x leverage, the liquidation probability stays below 5% and declines daily as your position matures. This is a fundamentally different risk profile from pool-based leveraged strategies where liquidation is an always-present, always-opaque threat.

SmartCredit.ioвҖҷs Fixed Rate Leveraged Lido Staking automates the entire position. Fixed borrowing cost. Audited smart contracts. Real-time liquidation probability displayed before you commit.

Try the Leverage Calculator вҶ’

Understanding What Drives Your Yield: Variables That Affect APY

The APY ranges above are real, but they are not fixed guarantees. The following variables influence your actual returns:

Total platform borrowing volume. SMARTCREDIT bonus rewards are shared proportionally among all active borrowers. If total open loan volume is below $5M, your share of the weekly 2,885-token reward pool is larger. As volume grows, individual reward shares decrease вҖ” but base interest income remains fixed regardless.

Total platform lending volume. The same principle applies to lender bonus rewards. Lower total deposits into Fixed Income Funds means higher reward APY per lender. As lending volume scales, reward dilution increases.

Reward caps. Borrower bonus rewards are capped at 10вҖ“75% APY (based on open loans). Lender bonus rewards are capped at 10вҖ“50% APY. These caps prevent runaway reward inflation while still delivering meaningful yield enhancement.

SMARTCREDIT token price. All bonus rewards are denominated in SMARTCREDIT tokens. If the token price rises, your USD-denominated return increases. If it falls, your USD return decreases вҖ” even if your token reward count stays the same. Strategies 3 and 4 are most sensitive to this factor; Strategies 5, 6, and 7 are also exposed but to a lesser degree since base lending/borrowing income is in stablecoins or ETH.

Staking pool size. Weekly staking rewards (4,327 SMARTCREDIT) are divided among all stakers. Fewer stakers means higher individual returns. This dynamic rewards early and consistent stakers disproportionately.

For a broader perspective on DeFi passive income methods and how SmartCredit.io compares to the wider market, see our comprehensive guide: How to Make Money with DeFi in 2025: 9 Proven Strategies.

How DeFi Passive Income Research Validates SmartCreditвҖҷs Model

SmartCredit.ioвҖҷs earning model reflects broader trends in sustainable DeFi yield. Independent research from DeFiLlamaвҖҷs lending protocol tracker consistently shows that platforms offering fixed-rate, term-based lending maintain more stable TVL and user retention than variable-rate pools вҖ” because predictable income attracts long-term capital, not just rate chasers.

Similarly, academic analysis on DeFi tokenomics published on platforms like SSRN confirms that reward programs layered on top of base yields вҖ” like SmartCredit.ioвҖҷs SMARTCREDIT bonus reward system вҖ” generate significantly higher user retention and capital deployment than single-layer yield products, as long as the base utility of the token (staking, governance, fee rebates) is maintained.

SmartCredit.ioвҖҷs multi-layer model вҖ” fixed base yield + token rewards + staking on those rewards + referral fees вҖ” is precisely this structure. The compounding effect of stacking four income streams is what produces headline numbers like 55вҖ“60% APY from what are fundamentally conservative, fixed-rate financial instruments at the base layer.

Frequently Asked Questions

What is the minimum amount needed to start earning on SmartCredit.io?

You can start lending or borrowing with as little as $100 in supported assets. For the First Loan Reward (Strategy 8), you need a loan of at least $1,000. For Leveraged Lido Staking, the minimum is 1 ETH.

Do I need to KYC or create an account to earn?

No. SmartCredit.io is non-custodial and permissionless. Connect your Web3 wallet (MetaMask or WalletConnect) and you can access all earning strategies immediately. There is no KYC, no account registration, and no custody of your assets by the platform.

How are SMARTCREDIT bonus rewards distributed?

Bonus rewards for borrowers and lenders are calculated weekly and allocated every Sunday at 12:00 UTC. They become claimable immediately via the вҖңMy RewardsвҖқ screen in the SmartCredit.io application. Staking rewards have a 90-day lock period before becoming claimable.

Can I earn on SmartCredit.io if I only hold SMARTCREDIT tokens?

Yes вҖ” Strategy 7 (staking) is available purely for token holders. Stake your SMARTCREDIT and earn 40вҖ“80% APY in additional tokens, distributed from the 4,327 weekly reward allocation, without any borrowing or lending activity.

What is the gas cost of participating in these strategies?

Gas fees are charged only on your first borrowing transaction. All subsequent borrowing transactions on SmartCredit.io are gas-free. Gas-less re-staking allows you to compound rewards weekly without additional Ethereum transaction costs.

Are these APY figures guaranteed?

No. APY figures are estimates based on current platform parameters, stable SMARTCREDIT price assumptions, and reward pool sizes. Actual returns vary with platform volume, SMARTCREDIT price movements, and reward cap thresholds. This article is for educational purposes only and does not constitute financial or investment advice.

Getting Started: Your First Steps on SmartCredit.io

Getting started takes less than five minutes:

- Visit smartcredit.io and connect your MetaMask or WalletConnect-compatible wallet.

- Choose your strategy. If you want passive income with zero complexity, start with Strategy 6 (lend and earn) or Strategy 7 (stake SMARTCREDIT). If you want to maximise yield actively, explore Strategy 3 or the Leveraged Lido Staking product.

- Review your terms. Fixed rates and fixed terms are displayed before you commit. There are no hidden fees and no rate changes after the fact.

- Set up Telegram monitoring. Connect your wallet to SmartCredit.ioвҖҷs Telegram Positions Monitoring System (via Profile вҶ’ Settings) to receive real-time alerts on any position requiring action.

- Claim and re-stake rewards weekly. Every Sunday, your bonus rewards are distributed. Claim them and use gas-less re-staking to compound without fees.

рҹҡҖ Ready to Start Earning? Choose Your Strategy.

Fixed rates. Non-custodial. No KYC. 9 earning strategies. Up to 80% APY. Start in under 5 minutes.

Disclaimer: This article is for educational purposes only and does not constitute financial or investment advice. Crypto assets and DeFi protocols involve significant risk including potential loss of principal. Always conduct your own research and assess your personal risk tolerance before participating in any DeFi strategy.