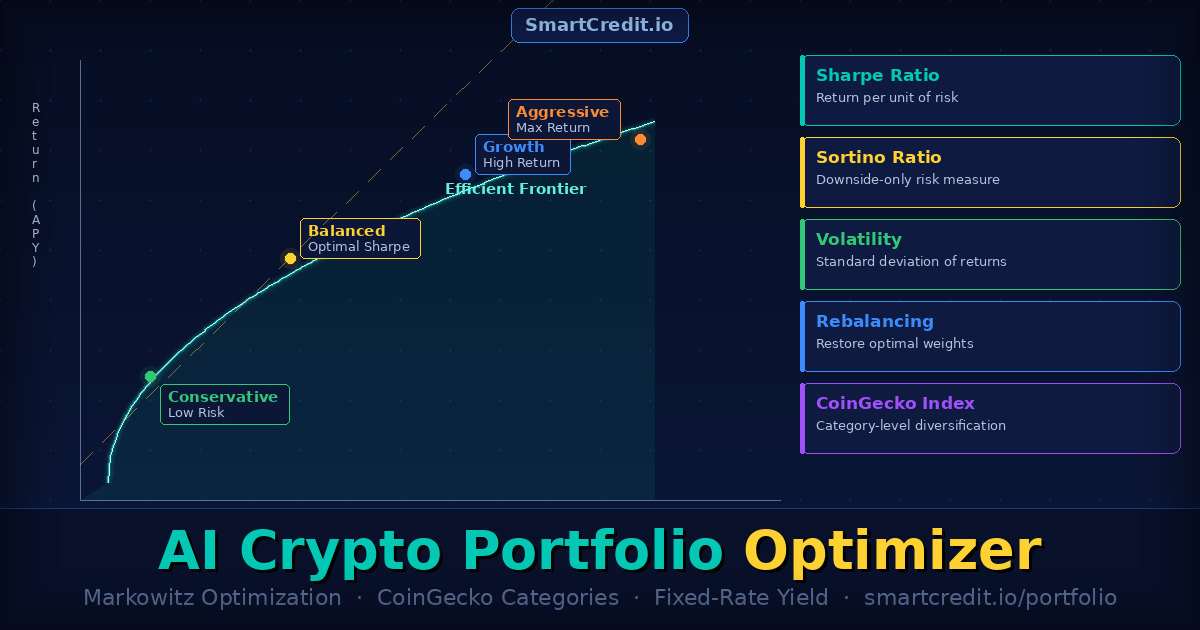

AI Crypto Portfolio Optimizer: Build a Markowitz-Optimized Portfolio Using CoinGecko Categories

Build optimal crypto portfolios using Modern Portfolio Theory: SmartCredit.io’s AI chatbot analyzes 15 CoinGecko categories (DeFi, Layer-1, Layer-2, Meme, Gaming) and calculates Markowitz-efficient frontiers. Input: risk tolerance (conservative/moderate/aggressive). Output: asset allocation maximizing Sharpe Ratio (return/volatility). Example: Conservative portfolio = 40% BTC, 30% ETH, 20% stablecoins, 10% DeFi, projected 12% annual return, 18% volatility. Plus: SmartCredit fixed-rate yield (8-15% APY) on holdings. Metrics explained: Sharpe Ratio measures risk-adjusted returns, Sortino Ratio focuses downside risk. Why rebalance quarterly: maintain target weights, capture gains. Free AI optimizer at SmartCredit.io. Visit