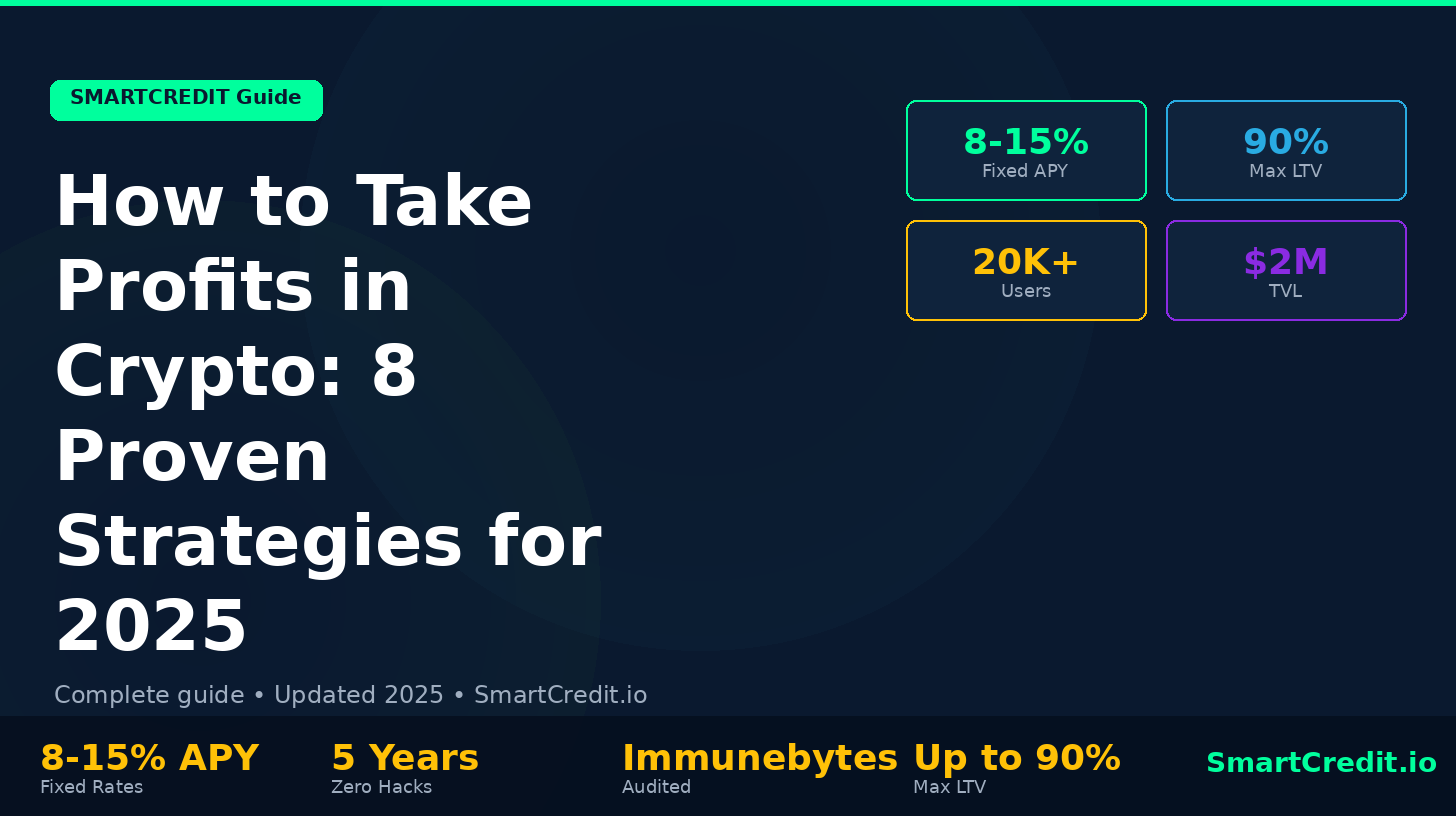

How to Take Profit in Crypto Without Selling: Tax-Free Liquidity Guide 2026

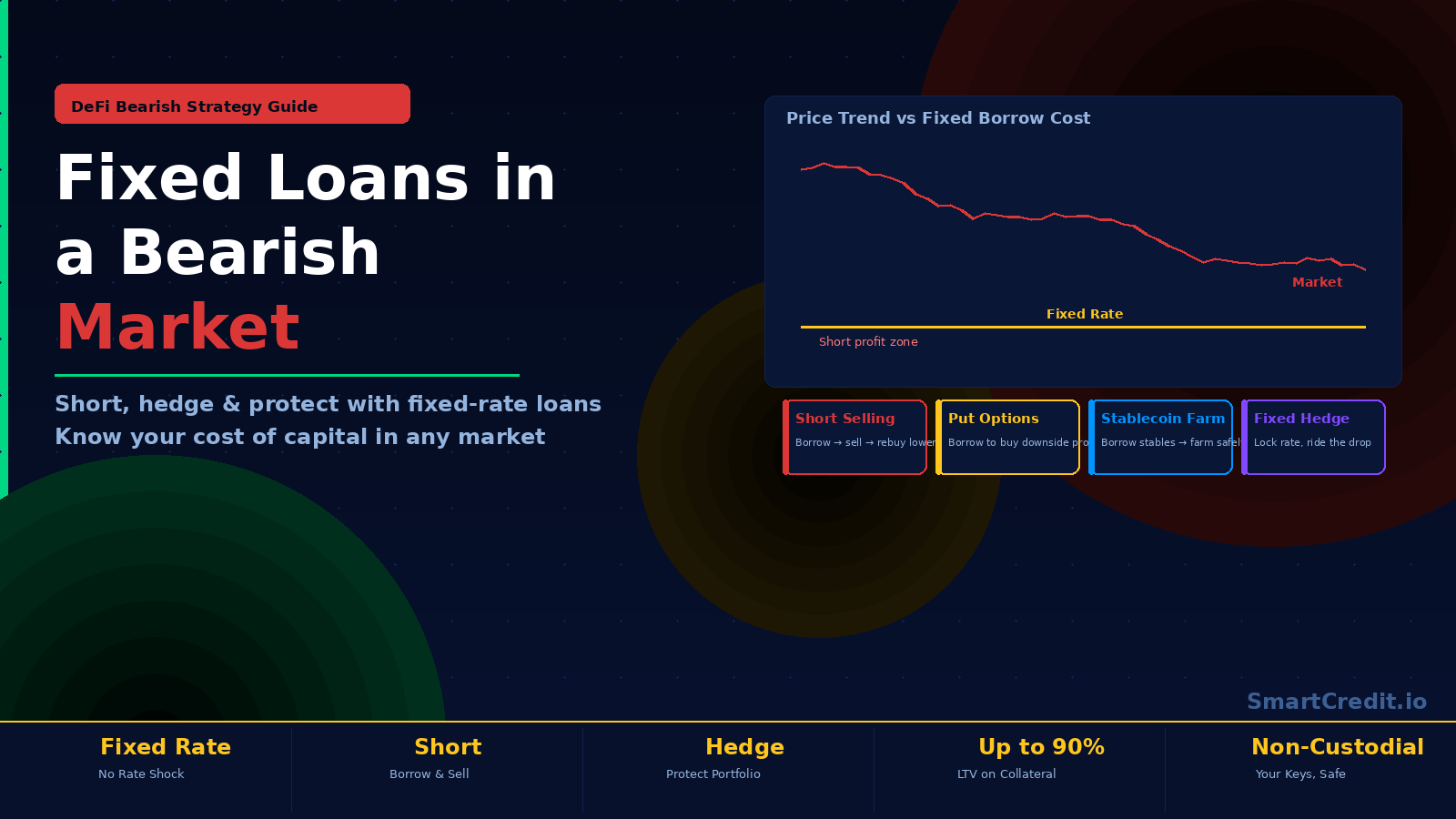

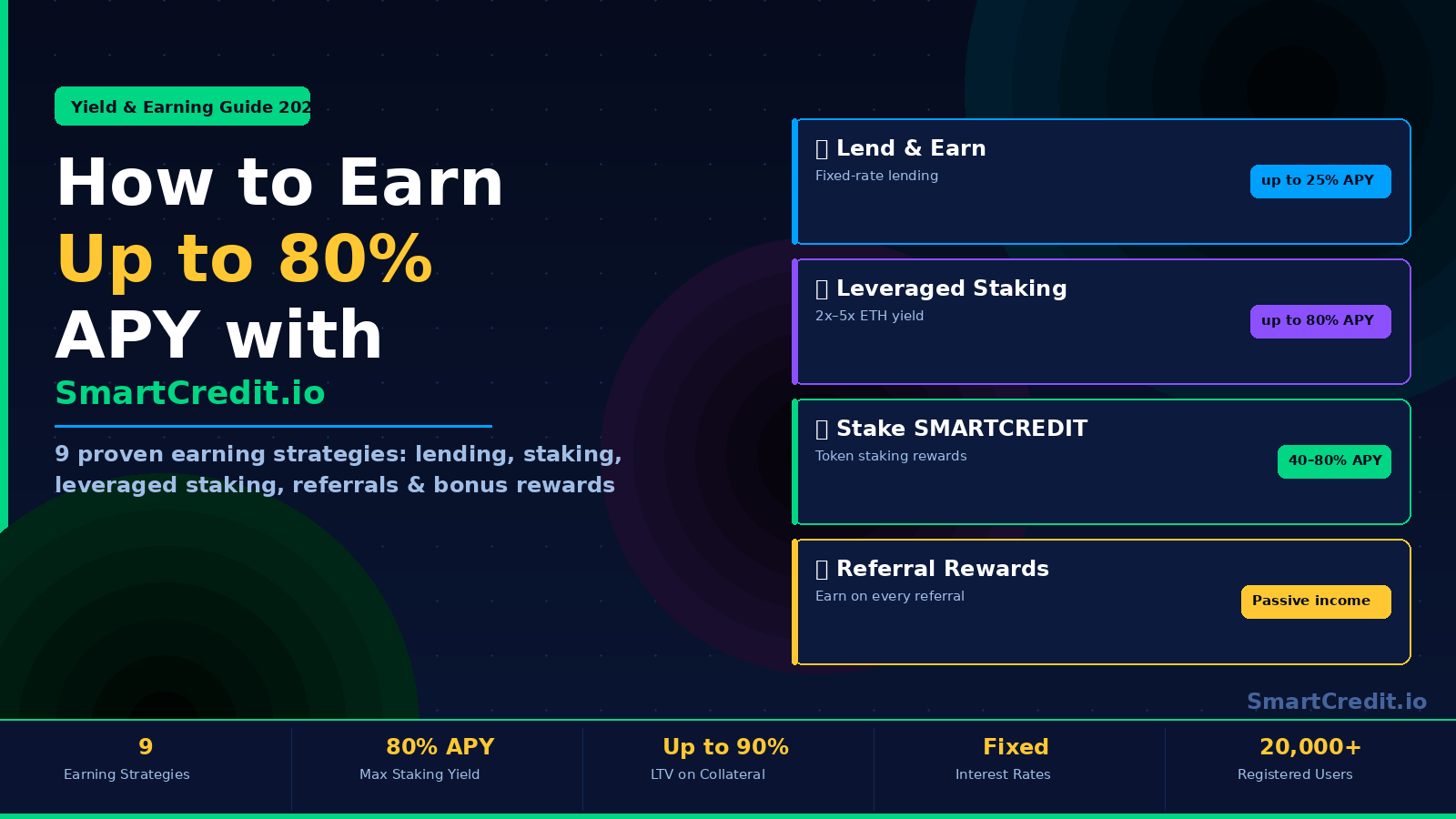

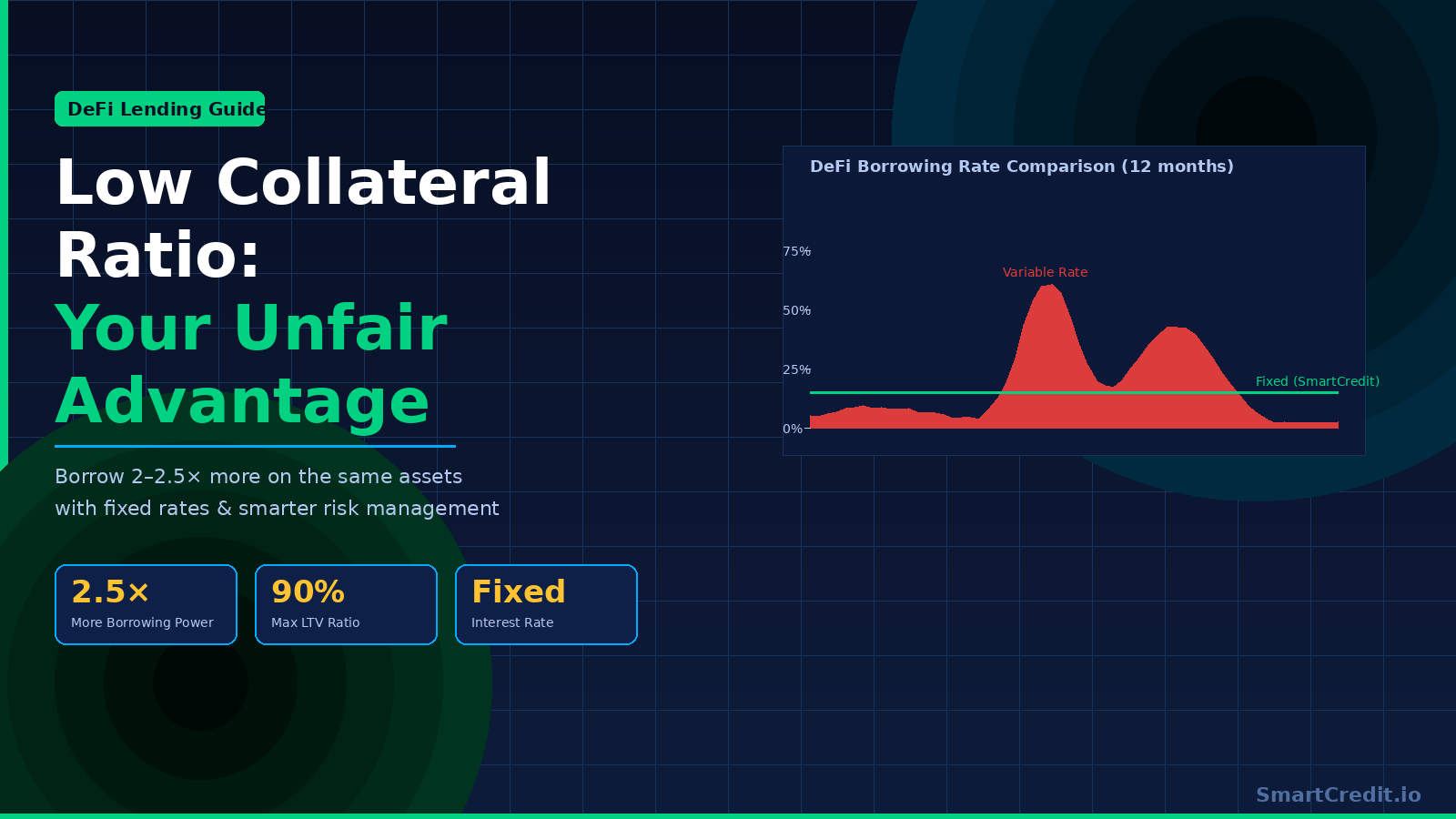

Access crypto gains without selling: borrow stablecoins against appreciated crypto on SmartCredit.io at 8-10% fixed APY, avoid 15-37% capital gains tax. Example: $80K portfolio, borrow $72K USDC at 90% LTV, pay $7.2K annual interest vs $27K tax on sale. Keep 100% upside exposure if market continues rising. Three strategies: (1) Tax-free liquidity – borrow against ETH/BTC, (2) Partial profit-taking – rotate 50% to stablecoins earning 12% APY, (3) Basis trading – arbitrage spreads. Real data: 2025 bull run, users saved average $18K in taxes using crypto-backed loans. SmartCredit: Immunebytes audited, non-custodial, 5-year zero-hack record. Visit /borrow