Credit-money is a very old concept. However, during presentations about money, we usually hear that money has to be durable, portable, divisible, and fungible. We fully agree with this distinction. But we don’t hear about the “credit-money”.

Money doesn’t have just one dimension, it has two — the base money and the credit money. The notes and coins in your wallet are the base money. The money that you have in your bank account is credit money.

This article:

- Analyses how base money and credit money work today.

- Analyses how base money and credit money worked in the last 5’000 years.

- Discusses credit money in the crypto sphere.

Below is a picture of the first known credit money, from Mesopotamia, from ca 2’500 B.C., now in the possession of the British Museum in London:

The intuitive answer to the key question of this article will be — yes. Since credit money has been around for so long, it will be around in the future as well.

But how?

The crypto sphere today does not have any form of credit money. Bitcoin, Bitcoin Cash, Ether, etc. can only be used as base money because credit money has to be dynamic. Credit money is elastic; it is created and destroyed every time we perform economic transactions.

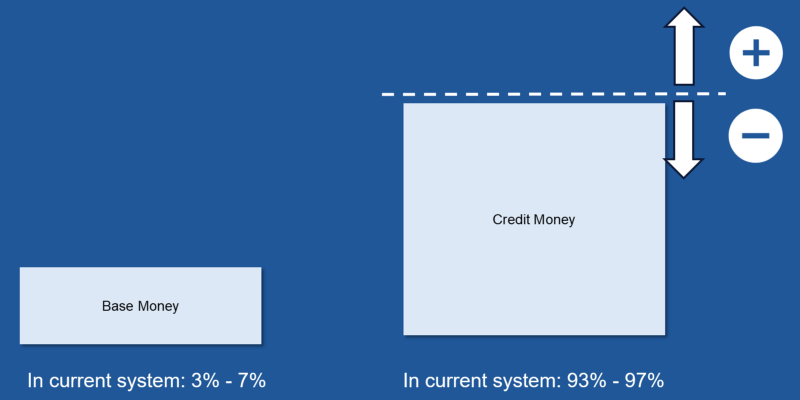

Base money versus the credit money

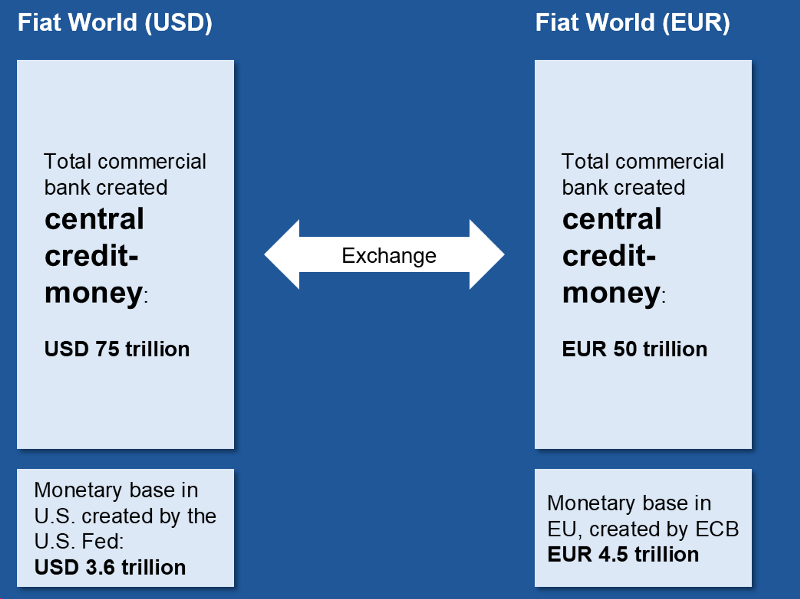

Let’s start with how they work today. Base money is created by central banks and credit money is created by commercial banks. Base money constitutes about 3% — 7% of today’s money, the rest is credit money.

Credit money is elastic, it’s amount grows and declines together with economic transactions. More economic transactions result in more lending which results in more credit money and vice versa.

This elasticity parameter is the key reason why we say that Bitcoin, Ether, etc. are not a form of credit money, but base money.

The supply of credit money also rises and falls — additional economic activities lead to an additional demand for credit and reduced economic activity to reduced demand.

Credit money is, by principle, rather temporary. However, in our current monetary system, we create more credit money than we destroyed, resulting in the continuous growth of the total credit money available circa 5% — 7% per year.

How is credit money created today?

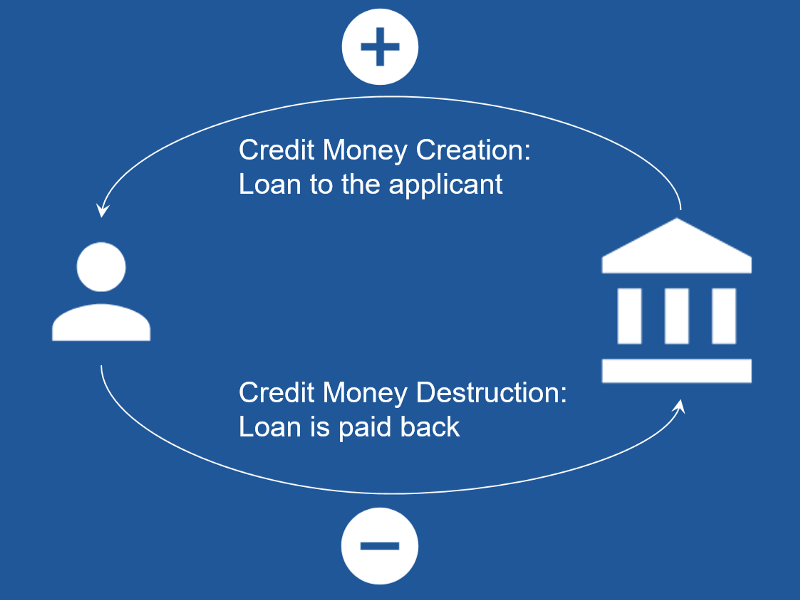

Credit money is created by commercial banks in the lending process (no, commercial banks are not lending your grandma’s deposits, they create credit money by the so-called “balance sheet extension” procedure).

Credit money is created every time you receive a loan from a bank and destroyed every time you pay back a loan. The money, which you have in your bank account, is not as durable as you might have thought — there are continuous cycles of destruction and creation happening in the background.

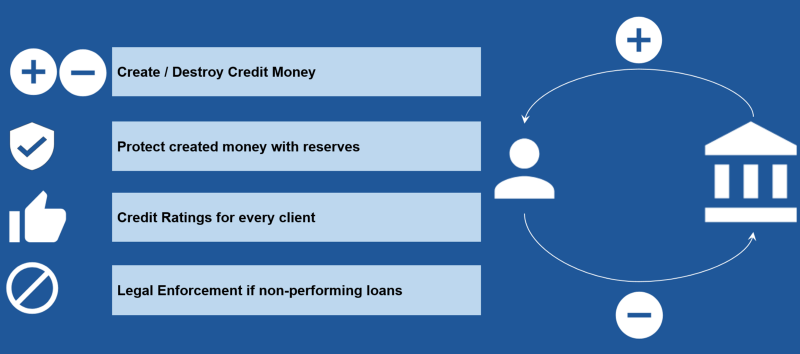

Banks create credit money and protect it with their reserves (for example, the Deutsche Bank which has a balance sheet to equity ratio of 100:1) and there are national deposit insurances as well (for example, the Swiss deposit insurance, which has reserve funds to cover 4% of all Swiss deposits).

In practical terms, banks do the following:

Banks protect the value of the credit-money which they have created with this mechanism.

Well, what happens if this mechanism fails? No problem, it’s fixed by creating more of the same (creating more credit money):

- The central banks will create additional base money and push it into the circulation via commercial banks. (Quantitative Easing) or

- Lending criteria are simplified (for example, Federal Reserve interest rate is reduced or the balance sheet to “mark to model equity” requirements are relaxed) so that more and more credit money will be created via lending. Or

- Governments will take on more debt and try to pump it into the real economy to stimulate the multiplication effect (this only works in cases of real investments, doesn’t work in cases of just spending).

This mechanism will result in inflation (sooner or later) or deflation (if no-one wants to borrow anymore), but as this happens later, then this is someone else’s problem.

Some people say that this system reminds them a little of the “musical chairs game”. We think that’s wrong — it IS the musical chairs game.

Monetary systems now and in the past

Monetary systems have always been made up of base money and credit money. The differences lie in:

- Who is creating base money?

- Who is creating credit money?

Our current fiat monetary system is not very old, it started in the period between the Federal Reserve creation (1913) and the gradual gold standard abolishment (1933 — nationalizing gold in U.S., 1944 -Bretton Wood agreement, 1971 — removing gold backing from USD base money, 1992 — removing gold backing from CHF base money).

Our fiat system looks as follows:

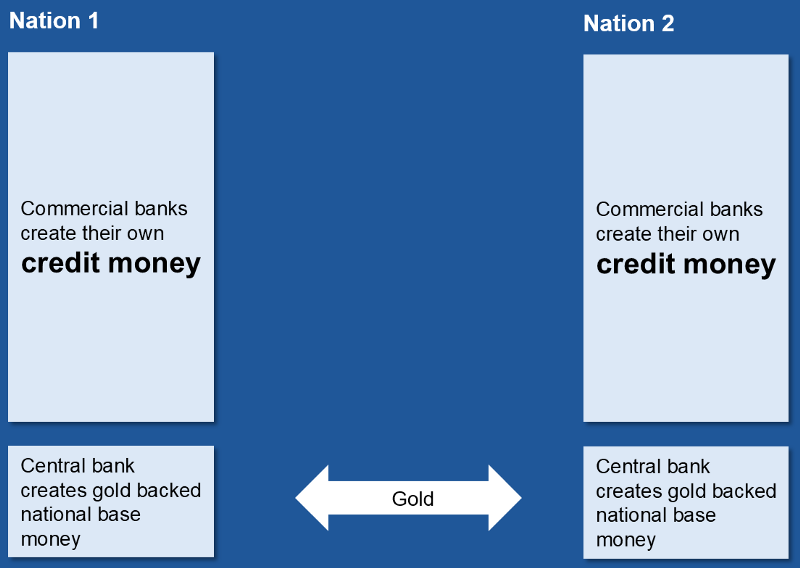

How did it work before our fiat system? Through the following:

- Practically, commercial banks created their own private credit money, which was exchangeable for physical gold.

- Central banks created the national base money, which was backed by and exchangeable for gold.

This system started to emerge around the time of the creation of the first central banks (in Sweden and England in the 1660s) and lasted until the Federal Reserve was created in 1913.

There were several sub-phases during this time — free banking areas, gold-based systems, some countries introduced central banks earlier, some later. In some cases, the central banks were “independent”, in other cases there were state treasuries, etc.

The key to this phase was however

- Base money was backed by a commodity — gold.

- Commercial banks created their own private credit money, which they protected with their reserves.

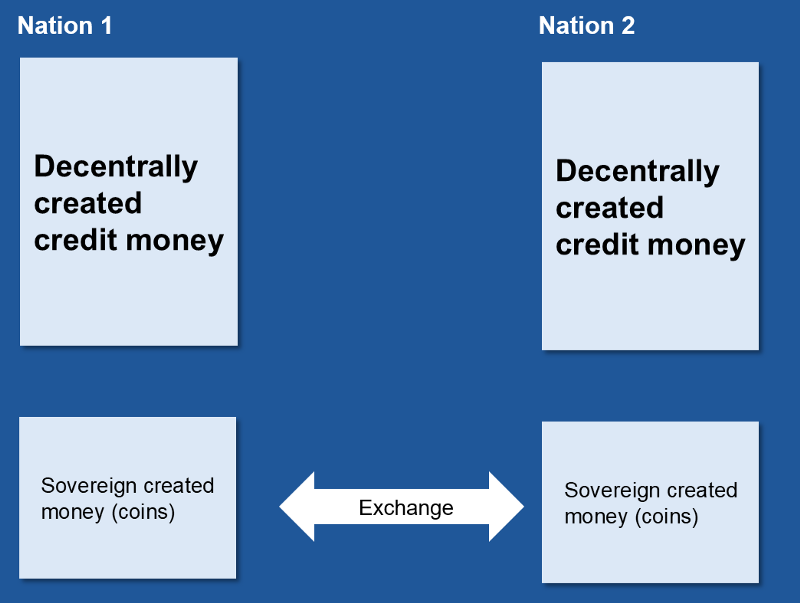

The earlier phase started around 500 B.C. and lasted until 1660. The first coins were created around 500 B.C. — this was the time when the standing armies in Europe, India, and China had to be financed — they were financed with sovereign minted coins.

In the beginning, the coins were usually 100% gold or 100% silver. Then later the kings started to reduce the ratio of precious metals in the coins — this caused hidden inflation in base money. However, the coins were legal tender and one had to accept them.

This was the time when the Phoenicia, Islamic Trading Network, Mediterranean, and Hanseatic Trading Networks existed. Decentralized credit money was created, in peer to peer transactions. Obligations to pay were used as bearer notes which could be used to pay third parties, who could pay fourth parties, and so on. In the end, the borrower had to pay to the owner of the bearer note.

So, the key to this phase was:

- Base money was created by sovereigns and was inflated slowly.

- Credit money was created decentrally by people in peer to peer transactions.

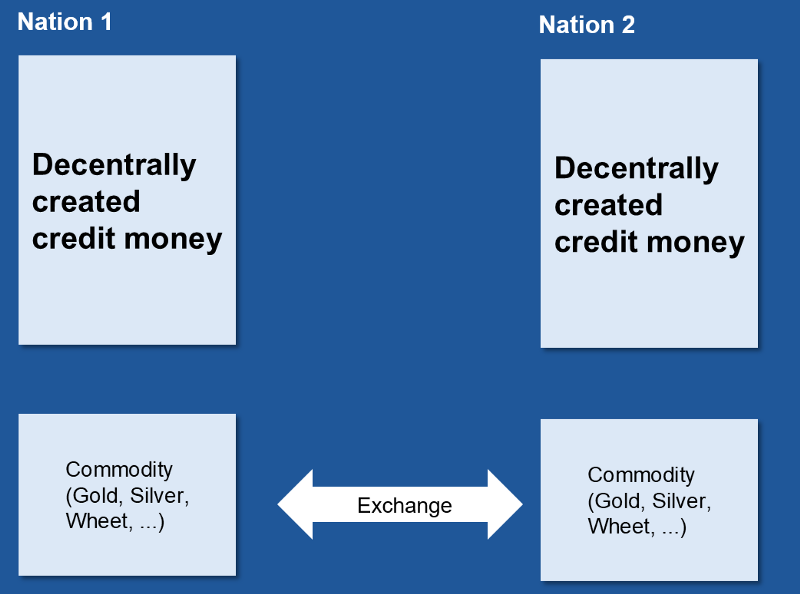

But how did it all work before 500 B.C? There were many blossoming civilizations during that time and the following are common to all of them:

- Commodities — gold, silver, grain, shells — were used as base money.

- Credit money was created decentrally.

However, governments and sovereigns were not involved in the definition of what the base money had to be — the people decided it. Neither did they define how credit money had to work — the people also decided it. There was no government involvement. But there was a court system for enforcing contracts. And there was a government system for enforcing the court’s decisions.

The first known credit money is from Mesopotamia, from about 5’000 years ago. It was created decentrally, in peer to peer transactions. Mesopotamia used grain as their base money — the unit of account was a barrel of grain. On top of this was the decentralized peer to peer credit money, in this case, clay plates with the stamps of the borrowers.

The barrels of grain were not easy to use in daily transactions. This facilitated the usage of clay plates based on credit money even more.

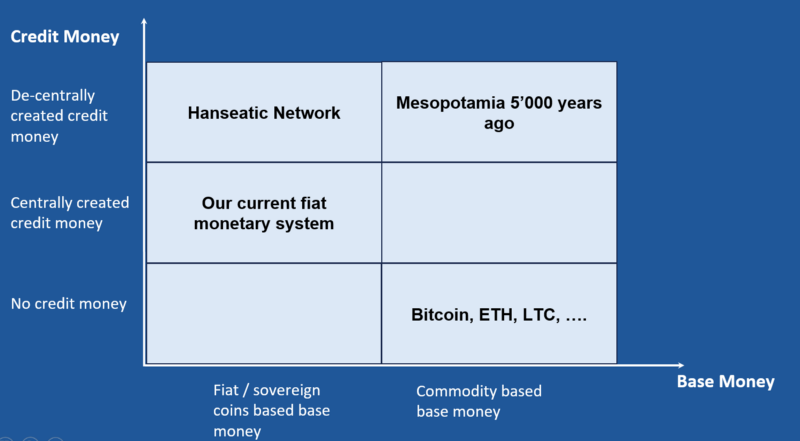

Classification of the monetary systems

By using base money and credit money dimensions we can classify the monetary systems of the last 5’000 years as follows:

The current crypto sphere doesn’t have the credit money approach, but none of the civilizations in the past has survived without credit money. Which leads us to the next question:

How will it work in the future?

The first conclusion is that credit money has been always there. It has been created either as:

- Decentralized peer to peer transactions

- Private credit money of commercial banks

- Central credit money of commercial banks

The second conclusion is that we are presented with two different possibilities to create base money:

- Controlled creation of base money — in this case, it’s created by central banks or sovereigns.

- Uncontrolled creation of base money — in this case, commodities like gold, silver, or grain are used as base money.

Uncontrolled creation of base money means that a commodity, which cannot be manipulated, will be used as the base currency. The Swiss National Bank has increased its amount of base money by 10x in the last 10 years since the Lehman crisis. One cannot do this with commodity-based base money.

U.S. Courts have defined Bitcoin as a commodity. Some people are unhappy about this. However, we are very satisfied with this — it allows us to move back to the commodity-based monetary systems (which are then by definition, non-manipulatable).

But what’s about the crypto credit-money? If we use the Bitcoin as our base money, who will create crypto credit money? In the end, there are 3 possibilities — decentralized credit money, privatized credit money, or centralized credit money.

Summary

Credit-money has been around for the last 5’000 years. No key civilization from the last 5’000 years has survived without using elastic credit money of one form or another.

But credit money is currently missing in the crypto sector. Bitcoin, Bitcoin Cash, Ether, etc. have the characteristics of base money. They are missing various characteristics, the elasticity, the continuous creation, and destruction, and more of credit money.

So, who will create elastic credit money for the crypto sector?

- Will it be created by the existing commercial banking infrastructure? Probably not since the crypto sector will not accept the “old world credit money”

- Will it be created decentrally without commercial banking? Probably yes!

Our thesis is that the pendulum will move back to where we started:

- We will have commodity-based base-money (Bitcoin, Ether, …)

- We will have decentrally created elastic credit money

- The court system will be there for enforcing the agreements

- The government will be there to implement the court’s decisions

It will be the same as it was in Mesopotamia 5’000 years ago. But this time empowered by the blockchain.

Additional Info

Please have a look at our other blog articles and our YouTube channel with many webinars and presentations.