SmartCredit.io is a decentralized finance loan marketplace. The focus of the platform is on:

- Fixed-term/Fixed-interest loans for borrowers — borrowers will know their cost of capital in advance and have predictability.

- Fixed-income funds for lenders — lenders define into which maturities they want to invest, and SmartCredit.io will make all the investments.

We are happy to announce the SmartCredit.io Release 1.2!

The key features of our new release are:

- Credit lines for borrowers

- Staking for holders (30–80% APY)

- Bonus rewards for borrowers and lenders (10–50% APY)

- New collaterals and new assets — ETH, wETH, wBTC, and partner tokens

- Fiat on-ramp/Fiat off-ramp for connecting with TradFi

- Positions Monitoring System

We hope you enjoy our new release and its exciting new features!

About SmartCredit.io

Most borrowing/lending platforms offer variable-rate, variable-term loans for borrowers. We are the opposite — we offer borrowers fixed interest rates and fixed terms.

This is important because of the cost of capital. Borrowers want to know their cost of capital, and lenders want to know how much they will earn. Both sides will have predictability.

Additionally, we offer DeFi fixed-income funds for lenders. The lenders define what kind of loans they want to invest in — they describe their investment rules. Every lender can choose whether to prefer short-term lending strategies (with less interest) or long-term lending strategies (with more interest) and how much of their portfolio to invest in the shorter term and/or longer term.

SmartCredit.io does in-the-background automated matching of borrowers’ loan requests with lenders’ fixed-income funds. Not only this, but SmartCredit.io monitors the loan, and if the borrower is not paying or the borrower’s collateral value sinks too much, the loan is liquidated.

SmartCredit.io never earns on liquidations — what’s remaining is transferred back to the borrower. This is one of the key differences from our competitors (Aave, Compound, and Maker). Our competitors earn revenues while liquidating the under-collateralized borrower because the collateral is sold at a discount, and the remainder of the collateral value becomes the profit of liquidator bots. Most of these bots are hosted by the respective platforms. In some months, the liquidation revenues transfer into the platform revenues, even into 50% of the respective platforms’ revenues.

As we said, SmartCredit.io is different. The remaining funds from liquidations are transferred back to the borrowers. SmartCredit.io does not earn on the borrower’s liquidations. If the collateral does not cover the borrower’s obligations, the loss-provision fund will pay the gap to the lender.

Many borrowing platforms (custodial or noncustodial) use the peer-to-pool-to-peer business model, meaning they pool the retail client assets and then lend to borrowers from these pooled assets.

Although this sounds common sense, this approach automatically classifies the investment product as a security, which means it must be registered by the SEC and other regulators. Also, the provider of this product — be it a DAO or a limited company — will need to register as an investment company (sometimes called an investment fund manager).

All peer-to-pool-to-peer business models now have regulatory challenges because they pool retail client assets and offer yield on the pooled assets. SmartCredit.io is different. It does not pool client assets — it’s a pure peer-to-peer play. While our competitors will need to register as security (and they will never get this registration), we are free from these requirements.

Credit Lines

Before our current release, every loan was a separate transaction — the borrower had to transfer collateral, receive the funds, pay back the loan, and receive his collateral back.

However:

- The old system was connected with the confusing “Approve ERC20” transactions.

- Many borrowers are not borrowing just once; they do this regularly.

- They want to transfer collateral once or add more later.

- Furthermore, borrowers want to take multiple loans without transferring collateral every time.

That’s why we introduced credit lines for borrowers. There are a few changes to the user interface. The main changes are in the background — a credit line will always be created in the background.

A credit line allows:

- Borrow multiple times against collateral

- Have diverse types of collateral in one credit line

- It’s like a “TradFi line of credit.”

When using a credit line, the user has to pay gas for:

- Creating his credit line

- Depositing collateral into his credit line

- Repayment of the loan

However, the user does not need to pay gas for any following borrowing transactions!

As ETH and ERC20 tokens are treated differently in Ethereum, the system will create a maximum of four credit lines per user in the background, depending on the selected asset and collateral.

- Borrow ETH, use ERC20 tokens as collateral

- Borrow ERC20 tokens, use ERC20 tokens as collateral

- Borrow ERC20 tokens, use ETH as collateral

- Borrow ETH and ETH as collateral — if someone needs it, it’s available.

If your loan is liquidated, the remaining assets will be transferred into your credit line, so you can use them as collateral later or to pay back the loans. Please note: SmartCredit.io does not benefit from your liquidations — that’s the big difference from all other lending platforms.

More info about the credit lines is available at: https://smartcredit.io/learn/how-does-it-work/credit-lines

Staking

Here is a summary of the staking rules:

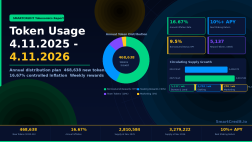

- Every week, 4,327 SMARTCREDIT tokens will be distributed as staking rewards.

- The staking rewards are pro rata, pro volume.

- The user must keep his SMARTCREDIT in staking for at least 90 days. If a user withdraws before 90 days, he will lose his rewards.

- If a user keeps his SMARTCREDIT in staking for 90 days or more, he is entitled to the rewards, including the rewards for the first 90 days.

- Staking rewards will be assigned every Sunday at 12:00 UTC.

- Staking rewards can be claimed via the “My Rewards” menu.

The staking returns depend on how many other holders are staking:

- The overall circulating supply is, at the moment of publishing, 1,547,381 SMARTCREDIT tokens.

- Ca 425,000 SMARTCREDIT tokens are allocated as liquidity in the exchanges and will not earn any staking rewards.

- If 50% of the remaining tokens are staked for an entire year, then the staking return is 40%+ annualized.

- If 25% of the remaining tokens are staked for an entire year, then the staking return is 80%+ annualized.

- The more other holders are staking, the smaller the staking return will become, and vice versa.

More details about the staking rewards are available in: https://smartcredit.io/learn/staking-and-rewards/staking

Borrower and Lender Bonus Rewards

Here is the summary:

- 2,885 SMARTCREDIT tokens are allocated for the weekly rewards.

- The rewards are pro rata and pro volume.

- If there are more borrowers on the platform than lenders, the lenders will receive more rewards, and vice versa.

- The rewards for borrowers and lenders are capped (in USD value). If there are weekly rewards above the cap, they are stored as “booster tokens.” The booster tokens are paid out later when the platform’s volume increases.

- Bonus rewards are assigned every Sunday at 12:00 UTC.

- The rewards are visible in the “My Rewards” section and can be claimed on the same screen.

More details about the bonus rewards are available at: https://smartcredit.io/learn/staking-and-rewards/borrower-and-lender-bonus-rewards

Variables That Influence the Yield

Borrower and Lender bonus rewards are allocated every week for the full seven days. The bonus and staking rewards per week are not fixed — they depend on several parameters.

- How many other users are borrowing — if the total borrowing volume (open loans) is more than the previous week, then the weekly rewards APY is smaller than the previous week. And vice versa.

- How many other users are lending — if the total lending volume (total deposits into FIFs without SMARTCREDIT token) is higher than the previous week, then the weekly rewards APY is lower than the previous week. And vice versa.

- The cap on the borrower and lender rewards — the cap on the borrower rewards in USD is 10%–75% APY (based on open loans); the cap on the lender rewards is 10%–50% APY (based on total FIF deposits without SMARTCREDIT token)

- The borrower/lender ratio on the platform — lenders will receive more returns if there are more borrowers. And vice versa.

- The number of booster tokens — if there are booster tokens and rewards APY is below the cap, then booster tokens will be used to increase the weekly rewards APY till the cap.

- How many other holders are staking — if there is less staking volume, then the staking rewards are higher because every week, 4,327 tokens will be shared between stakers.

New Collaterals and New Assets

SmartCredit.io introduces our partners’ tokens as collateral:

- EPAN — Paypolitan partnership

- PNT — pNetwork partnership

- pBTC — pNetwork partnership

Additionally, we included these tokens as collateral:

- SMARTCREDIT token — our token can now be used as collateral for borrowing

- wBTC

- ETH (Ethereum)

- wETH (Wrapped Ethereum)

- DAI

- USDC

- USDT

The new assets, which can be borrowed on SmartCredit.io, are:

- SMARTCREDIT token

- FRAX stablecoin

More info about the collaterals is in: https://smartcredit.io/learn/how-does-it-work/collaterals

Fiat On-Ramp/Fiat Off-Ramp

We integrated the fiat on-ramp/fiat off-ramp solution of our partner Mt Pelerin:

- Users can now convert from fiat to crypto and back in SmartCredit.io. For this, you need only a bank account in a TradFi bank.

- If daily transactions are below CHF 1,000 or monthly transactions are below CHF 15,000, any wallet can be used for the transfers.

- If the user has a higher conversion volume, the Mt Pelerin bridge wallet should be used. In this case, the KYC needs to be completed via the bridge wallet, which can be connected to SmartCredit.io via WalletConnect.

Positions Monitoring System

Every borrower can enter his profile and his telegram ID and subscribe to the SmartCredit.io bot. Borrowers would receive the following notifications:

- Notifications of upcoming loan repayments (if the borrower misses the repayment deadline, then the collateral is liquidated)

- Notifications if the liquidation probability of a specific loan has increased to 20% (user can then add collateral or repay parts of the loan)

Videos

- Video “SmartCredit.io Release 1.2 launched!“

- Video “How to earn 50% + with borrowing?“

- Video “How to earn 30% + with lending?“

- Video “How to earn 15%+ on your collateral value?“

- Video “How to earn with staking?“

Additional Information

Follow SmartCredit.io on Social Media

- Telegram: https://t.me/SmartCredit_Community

- Twitter: https://twitter.com/smartcredit_io