Crypto Monetary System – Why do we need Crypto Credit-Money?

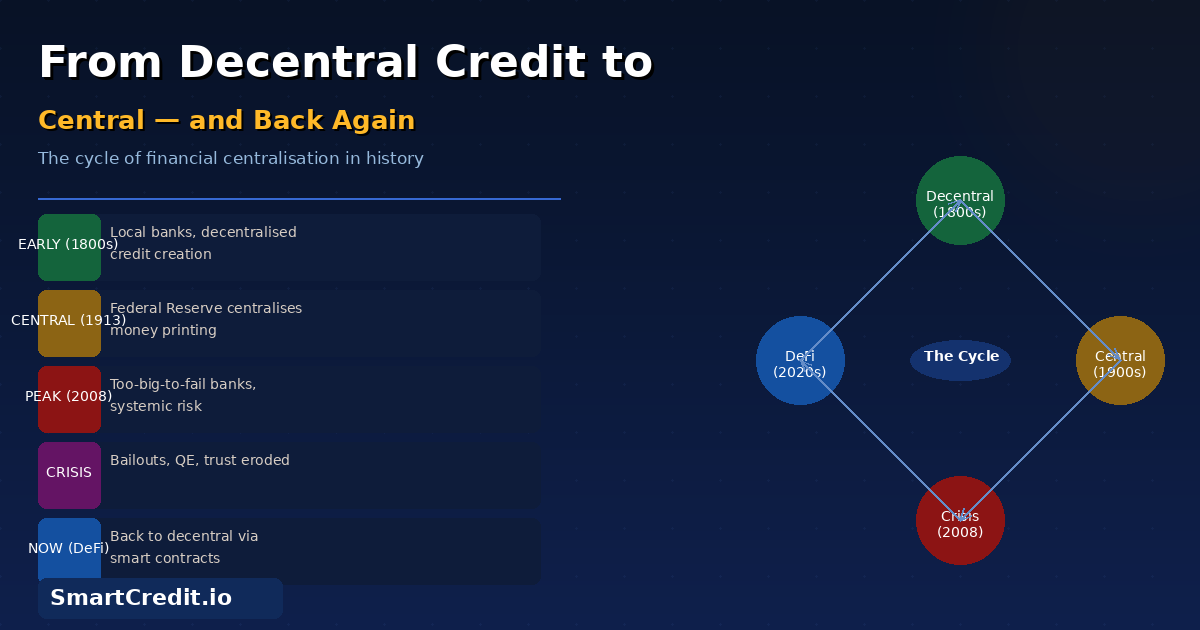

Crypto monetary systems enable peer-to-peer finance without banks. Core components: (1) Decentralized ledgers (Ethereum, Bitcoin), (2) Smart contract enforcement, (3) Algorithmic interest rates, (4) Collateralized lending. How it differs from fiat: no central banks setting rates, no fractional reserves, transparent on-chain transactions, global 24/7 access. SmartCredit.io provides fixed-rate stability (8-15% APY locked for 30-365 days) within this system, solving DeFi’s variable-rate volatility problem. Real data: Aave USDC rates ranged 3-38% APY in 2025. SmartCredit users locked 10-12%, avoiding 300%+ rate spikes. Immunebytes audited, 20K+ users, $2M TVL. The future: programmable money, algorithmic monetary policy. Visit